TNN

TNN(This story originally appeared in  on Dec 03, 2020)

on Dec 03, 2020)

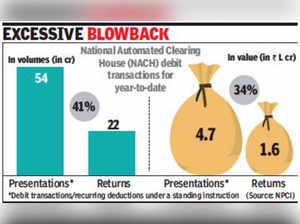

MUMBAI: Although most lenders have been reporting a collection efficiency of over 95% on their retail loans and lower than-expected delinquency following the pandemic, there are indications of stress among bank customers. Data from the National Payments Corporation of India shows that debit bounce rates among the National Automated Clearing House (NACH) transactions have gone up to 41% as against 31% pre-Covid. on Dec 03, 2020)A bounce takes place when a savings account does not have enough balance to meet recurring deductions under a standing instruction, which could be for utilities, insurance, mutual fund SIPs or loan repayments. This is not the same as a default or a delinquency, but an indication that the account did not have enough money as anticipated.

Bankers say that the nonsalaried and self-employed customers have been witnessing more erratic cashflows during the lockdown period as many businesses were affected due to the pandemic. According to a report by Macquarie, the collection efficiency (CE) numbers reported by lenders need to be taken with a pinch of salt given the bounce rates.

“While all the large banks have reported average CE of 95% for September, the bounce rates on NACH debit transactions have been inching up and currently stand at around 41% by volume and about 34% by value as compared to 31% and 25% in February,” Macquarie associate director Suresh Ganapathy said in the report.

The stress in the system is currently hidden as there is a Supreme Court order barring banks from classifying defaults during the Covid period as non-performing assets (NPAs) until further orders. If the stay on asset classification is lifted, lenders will need to classify delinquent borrowers as NPAs in the December-ending quarter.

According to a report by rating agency ICRA in November, the collection efficiency in ICRA-rated retail loan pools (originated largely by non-banking financial companies and housing finance companies) witnessed considerable improvement in September for almost all the asset classes. This was because of higher collections coming in the form of overdues and pre-payments.

“The improvement in collection can be attributed to sharper collection efforts of the lending institutions, ease in local restrictions, improvement in economic and business activity during July-September period and lowerthan-estimated impact of the Covid-19 pandemic in rural and semi-urban areas eliminating further rounds of lockdowns/restrictions at least so far,” ICRA said.

(Catch all the Business News, Breaking News Budget 2024 News, Budget 2024 Live Coverage, Events and Latest News Updates on The Economic Times.)

...moreDownload The Economic Times News App to get Daily Market Updates & Live Business News.

Read More News on

(Catch all the Business News, Breaking News Budget 2024 News, Budget 2024 Live Coverage, Events and Latest News Updates on The Economic Times.)

...moreDownload The Economic Times News App to get Daily Market Updates & Live Business News.